Taxation in the Context of Economic Security: Opportunities and Technologies [Mikhail Yuryevich Chernavsky] (fb2) читать онлайн

- Taxation in the Context of Economic Security: Opportunities and Technologies 994 Кб, 15с. скачать: (fb2) читать: (полностью) - (постранично) - Mikhail Yuryevich Chernavsky - Svetlana Nikolaevna Sayfieva - Nataliya Vladimirovna Vysotskaya - Oleg Fedorovich Shakhov - Valery Pavlovna Nevmyvako

[Настройки текста] [Cбросить фильтры]

Svetlana Sayfieva, Oleg Shakhov, Valery Nevmyvako, Mikhail Chernavsky, Nataliya Vysotskaya Taxation in the Context of Economic Security: Opportunities and Technologies

International Journal of Recent Technology and Engineering (IJRTE) ISSN: 2277–3878 (Online), Volume-8 Issue-2, July 2019

Svetlana Nikolaevna Sayfieva, Oleg Fedorovich Shakhov, Valery Pavlovna Nevmyvako, Mikhail Yuryevich Chernavsky, Nataliya Vladimirovna Vysotskaya

Revised Manuscript Received on 30 July 2019. * Correspondence Author Svetlana Nikolaevna Sayfieva*, Market Economy Institute of RAS (MEI RAS), Moscow, Russian Federation. Oleg Fedorovich Shakhov, Russian Presidential Academy of National Economy and Public Administration (RANEPA), Moscow, Russian Federation. Valery Pavlovna Nevmyvako, Russian Presidential Academy of National Economy and Public Administration (RANEPA), Moscow, Russian Federation. Mikhail Yuryevich Chernavsky, Moscow State University of Technology and Management named after K.G. Razumovsky (first cossack university), Moscow, Russian Federation. Nataliya Vladimirovna Vysotskaya, National Research University Higher School of Economics (HSE), Moscow, Russian Federation; Russian University of transport (RUT (MIIT), Moscow, Russian Federation. © The Authors. Published by Blue Eyes Intelligence Engineering and Sciences Publication (BEIESP). This is an open access article under the CC-BY-NC-ND license http://creativecommons.org/licenses/by-nc-nd/4.0/Abstract: The aim of the present work is conducting the theoretical and legal analysis of threats and risks of tax security of the state, as well as developing on this basis measures to eliminate them and prevent their occurrence, improving methods of minimization, and neutralizing the possible consequences of their impact. To solve the set goal, the method of expert survey was used that allowed generalizing the concept of tax security, determining its economic, social, and legal nature, as well as defining the main risks and threats to the tax security of the state. The article substantiates the relevance of the study the issue concerning insurance of tax security of the state. Various approaches of scientists to the definition of the tax security concept essence were considered, which would satisfy the interests of all entities of tax relations. To determine the efficiency of tax administration to the benefit of the tax security, the main threats and risks of the tax security caused by external and internal factors are identified, as well as measures to eliminate them and prevent their occurrence are proposed. The authors propose the stages of tax risk management when constructing an effective system of tax security, as well as develop a structural and logical scheme of risk management of tax security of the state. Index Terms: tax security, economic security, tax policy, fiscal and regulatory functions of taxes, tax security indicators; tax risks, tax burden.

I. INTRODUCTION

Understanding the role of taxation in the provision of economic security includes consideration of its positive effect on macroeconomics (growth of the tax potential of the state), as well as negative aspects in the form of nonreceipt of tax revenues to the budgets of all levels, criminalization of tax relations, growth of tax nihilism, the crisis of the tax system, destroying the socio-political foundations of the state and depriving the authorities of financial resources. In the modern world, the importance of taxation is so great that the formulation of the tasks facing the tax policy without considering them from the standpoint of the relationship and mutual influence with the economic security, can lead to a loss of consistency and efficiency of the overall economic strategy, since taxes are objectively included in each of the elements, which are distinguished during strategy analysis, namely, — economic independence; — sustainability and stability of the national economy; — ability to self-development and progress [1], [2]. Economic independence implies the independence of the state in the formation and development of its own economic system and the implementation of foreign economic activity to the benefit of the people. Economic independence is possible only in the presence of all its metasystems, subsystems, elements, and components. At the same time, given the internationalization and globalization of the economy, any country in the world has to resort to measures to protect its own economic interests, of which taxation is the most effective measure. The sustainability of the national economy implies the ability of the latter to respond to changes in the external and internal environment through continuous improvement of the components of its internal structure based on the adaptation mechanism in order to achieve the goals of socio-economic development and the effective functioning of the national economy. The sustainability of the national economy is the main task of the macroeconomic policy of the state and an important condition for ensuring the economic security. This is expressed, first of all, in the formation of state policy aimed at supporting the national economy in a sustainable condition. The role of taxation in this process is most fully implemented through the regulatory function, which is the ability of taxation to coordinate, harmonize, organize, cooperate, and stratify social interaction and management. Taxation also affects various components of the economic system, namely: pricing, volume and growth rates of social production, sectoral structure and directions of capital migration, technical level of production, scope of research, labor demand and supply, level of employment and wages, consumption model, distribution of income in society, its social and regional differentiation, and conditions of foreign economic activity. The ability to self-development and progress involves the ability to choose state’s own development model, to carry out continuous modernization of production, effective investment and innovation policy, and to develop the intellectual and spiritual potential of the country. Taking the above into account, it should be noted that taxation occupies a special place in the economic security system since it not only provides financial resources to almost all components of the economic security (financial, social, environmental, legal, etc.) but also is a tool of the impact on economic and social processes.II. LITERATURE REVIEW

In the course of the interpretation of the essence and content of the tax security definition, it has been revealed that among scientists dominates the understanding of its economic and legal form, which should ensure the creation by the state of conditions allowing the interaction of the interests of the individual, business structures, and the state based on the principle of mutual responsibility of tax agents. Therefore, it is necessary to give a more meaningful and accurate definition of the tax security concepts developed by modern domestic and foreign scientists (Table I).Table I. Interpretation of the essence of the tax security definition in the scientific literature

From Table I it is evident that scientists understand the tax security as a form of security, which should provide the appropriate conditions for interaction among the state, business entities, and individuals to achieve the principle of mutual responsibility of business entities. The complexity of the study of this term is that the authors define differently the characteristics of this category. First, the tax security characterizes the status of protection of the taxpayers’ interests and those, who distribute the gross domestic product through the taxation system. Secondly, it is the ability of the system to perform its functions and to respond to any changes in a timely manner. Third, it is the ability to respond to risks and dangers, to eliminate, minimize, accept or ignore their impact on the participants of the tax security [8]. This concept is difficult to study, because, on the one hand, it characterizes a certain state of the system, which protects the interests of taxpayers and entities that are involved in the distribution of GDP through the taxation mechanism, while on the other hand, it is a certain characteristic of the system, which is able to ensure the timeliness of fulfillment of functions by the tax system, and adequately response to changes in the tax policy of the state under the influence of a combination of factors; the third point is the ability of the system to withstand risks and dangers, to optimize, and under certain conditions, to minimize their impact on all participants of the tax security.

III. METHODS

To solve the set goal, the method of expert survey was used that allowed determining the following main issues of the study: 1. generalizing expert opinions on the interpretation of the tax security concept; 2. defining the essence of the economic, social and legal nature of the existence of the national security. 3. identifying the main risks and threats to the tax security of the state. Managers and senior management of travel agencies (22 experts in total) were involved in the expert survey. During the expert survey, experts were asked to give their own interpretations of the tax security concept, to reveal the essence of the economic, social, and legal nature of the existence of tax security, as well as to characterize the main risks and threats posed to the tax security of the state. The results of the expert survey were used to propose a generalized structural and logical scheme of tax security risk management (Fig. 1). Fig. 1. Generalized structural and logical scheme of tax security risk management

Fig. 1. Generalized structural and logical scheme of tax security risk management

IV. RESULTS AND ISCUSSION

A generalization of expert approaches to the tax security concept is given in Table II.Table II. Approaches to the definition of the tax security concept

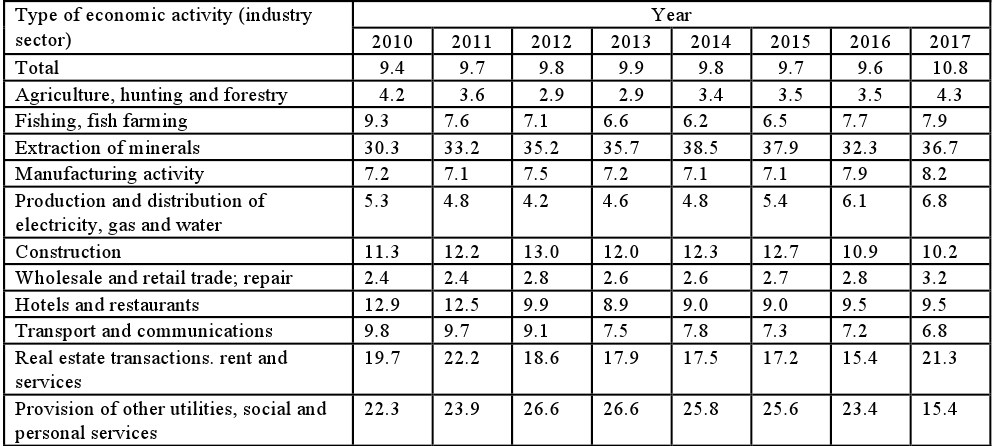

Thus, most of the interviewed experts (12 people) consider tax security as a subsystem of the state national security, which represents a certain status of the tax system. To develop a comprehensive view of the tax security level of the country, the economic, social, and legal nature of the tax security existence was analyzed. The economic aspect of the tax security, according to experts, is determined by the degree of fullness of the budget with financial resources, which is influenced by a number of factors: the level of economic development, GDP growth, inflation rate, the tax burden on the economy agents, which are involved in the reproduction. For better understanding of this aspect, it is necessary to figure out what the taxation effectiveness means, and how its level is determined. Tax efficiency can be calculated by comparing costs and benefits. The results can be considered as the amount of taxes collected by the state into the budget, while expenses include funds necessary to collect these taxes. However, if the payer has paid a large amount of taxes, this can lead to a decrease in activity among entrepreneurs and investors, or to the transition of the business into the shadow that will further lead to a decrease in tax revenues to the budget [9]. In the authors’ opinion, the viewpoint of Yuri K. (an employee of the Federal Tax Service) is the most rational. According to this standpoint "the harmonization of tax systems can be assessed to some extent both in terms of tax collection and the level of the shadow economy in the country. After all, only a country, where the level of tax collection is high enough while the level of the shadow economy is not so great, can be considered civilized and prosperous." While agreeing with the author's basic provisions it should be noted, however, that evaluation factors should not be neglected. It is necessary to take into account the quality and expert assessment of legislation in the tax system, which contains many problems and legal conflicts. Taking into account these indicators, it becomes clear that one leading indicator of the tax security is the level of the tax burden on taxpayers, which shows how taxes and fees affect both individual business entities and the economic condition of the state (Table III).

Table III. Dynamics of tax burden indicators in Russia by types of economic activity (according to the method of the Federal Tax Service of Russia*), %

* The calculation is made without taking into account income on consolidated social tax and insurance contributions for compulsory pension insurance

* The calculation is made without taking into account income on consolidated social tax and insurance contributions for compulsory pension insurance

The legal aspect of the tax security, according to experts, consists in the process of control over the tax system, creating conditions for fair taxation of social reproduction entities and declaration of conditions in the laws. In addition, regulatory provisions can be used to minimize abuses in the allocation of budget funds. The social aspect of the tax security, according to experts, consists in the degree of protection of the interests of all business entities, namely, the state, businesses and the population, through fair taxation, tax preferences, payment of taxes and the distribution of tax revenues among the agents of the financial system. The so-called tax culture and discipline should be formed, which will provide the necessary level of the tax security. One of the experts (Victor K., an employee of the city administration) notes that the social orientation of taxes should be manifested through the ratio of direct and indirect taxation. Moreover, direct taxation should prevail that will reduce the burden on consumers themselves, and in the case of effective tax rates will also activate the production process in the state. In addition, the expert continues, "the collected taxes should be effectively implemented to solve socio-economic problems to meet the interests of both the state and the population." Thus, in his opinion, only due to the sustainable development of the economy, society, and the rational use of budgetary funds, it is possible to achieve the necessary level of the TS, which will satisfy the interests of all subjects of taxation. However, all this is possible only with the functioning of an effective, efficient, and rational tax system. To determine the essence, methods, and construction principles of the economic nature of the tax security, the main risks and threats arising in the course of its efficient construction were determined during the survey. According to experts, the main source of the threat to the tax security is the tax risks, which should be understood as the probability of negative consequences for the tax system due to the inefficiency of its construction and functioning, the impact of existing threats, as well as external and internal factors. Thus, threats are a prerequisite for the occurrence of risks. The difference between them is that the risks are probable and can be measured quantitatively if they occur, while the threats are actually the existing dangers, which under the influence of factors encourage the occurrence of these risks, and their interdependence leads to financial losses for both business entities and the state, in particular, due to ineffective tax policy. To avoid the ambiguity of the concept of threat, the above-mentioned parameters should be defined both for the state (the entity that levies taxes) and taxpayers (the entities from which these taxes are levied). According to experts, the tax threats of the state include the following: a low level of tax culture, the existence of tax corruption, tax evasion, excessive expenses for the maintenance of the state tax bureaucracy, unjustified controversy in the current tax legislation, the growth of tax debt, and irrational use of taxes. The threats that taxpayers face include the following: uneven and unjustified distribution of the tax burden among business entities, a high proportion of economic entities that operate in the shadows, the outflow of national capital into the economy of foreign countries, and excessive interference of fiscal authorities in the economic activities of enterprises. Thus, the probability of negative phenomena for the tax security due to the inefficiency of the tax system, the action of existing threats, as well as the impact of external and internal factors should be considered as risks. That is, a prerequisite for the emergence of risks are threats. The main difference between these concepts is the following: the risk is likely to occur, and its occurrence can be measured, while the threat is already an established danger, which under the influence of certain factors leads to the occurrence of a certain risk. Their interdependence leads to losses for both the state and economic entities. The main risks and threats of the state tax security, identified according to the results of the expert survey, are presented in Table IV.

Table IV. Main risks and threats of the tax security of the state

Tax security is characterized by the ability of tax subjects to preserve the results of their activities under the influence of various external and internal threats and risks. The main goal of the state is to minimize tax risks by reducing the number of situations that pose threats to the tax security of taxpayers, society, and the economy in general. In turn, the business entities themselves should take into account the dangers and threats of their activities and will conduct economic activities as long as the results exceed costs. Otherwise, they will be forced to stop their activities, make certain changes to improve efficiency or move into the shadows that will have negative impact on the state, since business entities in their aggregate are the largest source of tax payments [10]. To ensure a sufficiently high level of social and economic life, it is necessary to take into account tax shortcomings, which are caused by inefficient and inadequate attitude of the state to taxpayers creating destabilizing factors in the tax system, namely, tax abuses and offenses, numerous tax evasions, and the use of intricate schemes of their collection [11]. All tax risks should be carefully studied and analyzed, while measures to eliminate them should be carried out, because in the case of a frivolous attitude to this issue, threats to financial security, in particular, and national security, in general, may arise. Taking into account the results of the conducted study and analyzing this problem for pragmatic reasons, tax risk management can be characterized as a process covering the following stages: — risk identification and assessment; — prioritization of risks; — work with risks, including the choice of methods to influence risks when comparing the effectiveness of the selected measures and decision-making; — assessment of work results with risks and management organization quality. Thus, the content of the tax risks management is defined as the process of identifying, assessing, and eliminating tax risks, preventing the possibility of their occurrence, improving methods of minimization, as well as neutralizing the possible consequences of their impacts. At that, tax risks may result in their possible negative impact on tax security or the problems created by these risks in the field of taxation. Ensuring the effectiveness of the tax risk management process requires its organization as a continuous cycle, which is based on an appropriate strategy taking into account the content and objectives of this process. The tax security risk management scheme, consisting of four successive stages, gives clear representation of this cycle performance: First stage: planning and definition; Second stage: risk analysis, assessment, and description; The third stage: risk neutralizing methods; Fourth stage: monitoring of means to prevent and counteract to risks. In this process, the main place is occupied by a combination of all the facts, circumstances and procedures relating to the organization of risk management to ensure the tax security of the state. A systematic approach to the essence of risk management and modeling of its functional and procedural characteristics has its advantages. Firstly, it allows effectively directing management actions (risk analysis, development of measures, etc.). Secondly, it helps to determine the logical interrelated sequence of actions to ensure the reliability of the relevant activities and the quality of the risk management organization in general. According to the proposed scheme, the quality monitoring of the risk management organization is carried out at different levels. At the first level, it is necessary to establish the effectiveness of a particular stage in the risk management process. At the second level, it is important to assess management by examining ways and means of achieving the objectives of the fiscal authorities. The third level concerns determining the quality of the risk management process organization in general to ensure the tax security of the state. Changes and development in the tax security system cannot be achieved without the perfection of information systems and analysis, improvement of scientific and technical potential, creation of information technologies, modernization of the taxpayer accounting system, application of new analysis and forecasting models by tax authorities, as well as without improvement of the payment accounting system [12]. Tax policy is the only one of the main tools for building an effective and efficient tax system, whose main task is to fill the budget with sufficient payments in the form of taxes, and their effective use. It is always difficult for the state to make the right decisions. Therefore, it is necessary to actively use the tax security indicators, which involves their calculations, subsequent analysis, and use of obtained data to build forecasts of the main indicators of the tax system. Correctly and timely calculated indicators will make it possible to have real figures on the economic development of the country [13], [14], [15]. The tax security is closely related to the level of tax culture, which is manifested in the observance by all subjects of tax legal relations of laws and other normative legal acts, timeliness and correctness of payment of taxes, knowledge of laws, their rights and obligations, as well as trust in the state in its effective redistribution of collected taxes and fees. It is trust and mutual cooperation among all subjects of tax relations that will give impetus to the development of tax culture, which is the basis for fundamental changes in the tax policy of the state, building an effective national economy, and ensuring reliable tax security of Russia.

Последние комментарии

13 часов 44 минут назад

17 часов 59 минут назад

20 часов 17 минут назад

22 часов 7 минут назад

1 день 3 часов назад

1 день 3 часов назад